MoneyViewTearDown

About MoneyView

MoneyView positions personal loans around speed, digital access, and low-friction application. The teardown uses the user-provided PM notes plus public product pages and official MoneyView visuals to frame the opportunity.

Business Signal

Product insight: as lending revenue scales, repeat-borrower clarity becomes a retention and portfolio-health problem, not only a marketing problem.

Problem Discovery

The highest-value problem is not simply "users need more money." The product problem is that active borrowers cannot see whether their repayment behavior has unlocked a responsible second-credit path.

Users may be restricted from taking another loan until an existing loan is fully or substantially repaid.

Even good borrowers do not know what amount is possible, when to reapply, or what action improves eligibility.

Users with urgent needs may switch lenders or take high-interest alternatives before MoneyView can help.

PM question How might MoneyView show active borrowers their next eligible credit path before they apply and fail?

User Personas

The teardown compares four borrower types, then focuses on Rajesh because his strong credit profile makes the issue clearly about product clarity, not just risk rejection.

Rohan Sharma

Software Engineer- Age / City

- 28, Bangalore

- Credit

- 780

- Need

- Laptop and certification course

- Pain

- Approval delays and short-term rates

Priya Mehta

Boutique Owner- Age / City

- 28, Mumbai

- Credit

- 690

- Need

- Inventory and seasonal cash flow

- Pain

- Second loan blocked while first is active

Anjali Roy

Freelance Designer- Age / City

- 26, Pune

- Credit

- 650

- Need

- Software and marketing investment

- Pain

- Thin credit history and income proof

Rajesh Kumar

Government Employee- Age / City

- 50, Chennai

- Credit

- 810

- Need

- Urgent medical funds with fewer formalities

- Pain

- Does not know if a second loan is possible

Rajesh Kumar, government employee

Rajesh is the best teardown lens because his excellent credit score removes "bad borrower" as the obvious answer. The product still needs to explain eligibility, amount, timing, and risk guardrails.

User Journey Map

The journey breaks when Rajesh applies before he understands eligibility. The failure point appears before disbursement, at the moment where the product could have explained the next action.

Identifies the need for an additional loan due to urgent medical expenses.

😟 AnxiousDoesn't know if he qualifies for another loan while repaying the first one.

Show real-time eligibility status within the app.

Researches lender policies on multiple loans and checks MoneyView's website and app.

🤔 UncertainNo clear information on second-loan eligibility or required conditions.

Provide a second-loan eligibility calculator in the app.

Tries applying for a second loan but gets rejected due to active loan.

😞 FrustratedInstant rejection with no explanation of why or when he can reapply.

Offer pre-approved top-up loans or explain eligibility criteria upfront.

Calls customer support to understand options for additional borrowing.

😠 AnnoyedSupport gives generic answers with no clarity on exact eligibility criteria.

Train agents to provide clear, personalized eligibility guidance.

Starts looking for other lenders or informal borrowing options.

😕 UncertainMay opt for high-interest alternatives or informal lending.

Offer structured second-loan plans or guide users toward better financial planning.

Receives a pre-approved top-up loan offer via app notification.

🙂 RelievedOffer comes too late after user already explored other lenders.

Proactively notify eligible users before they seek alternatives.

Accepts the pre-approved offer and receives the loan instantly.

😊 SatisfiedAppreciates the quick process but wishes he knew about it earlier.

Improve loan visibility and proactive communication to avoid frustration.

Pays adjusted EMI with the new loan structure.

🙂 ComfortableWonders if future top-ups will be available when needed.

Provide repayment tracking and guidance on future loan eligibility.

Pain Prioritization

Before choosing a solution, the teardown compares the three strongest pain points from Rajesh's journey, then uses RICE to identify which problem deserves the first product bet.

Borrowers may need more credit than the product can safely offer. This is painful, but changing limits depends heavily on risk policy and lending economics.

Users worry about cumulative EMI and interest over time. Important, but improving pricing is slower because it touches underwriting, partner terms, and portfolio margin.

Good active borrowers do not know if, when, or why they can access more credit. This is high-impact because it can be improved through UX, reason codes, and proactive eligibility communication.

| Pain point | Reach | Impact | Confidence | Effort | RICE |

|---|---|---|---|---|---|

| Loan amount restrictions | 4 | 5 | 4 | 3 | |

| High total interest payment over time | 3 | 4 | 5 | 3 | |

| Limited clarity on second-loan eligibility | 5 | 4 | 5 | 2 |

Decision: prioritize the clarity gap first because it has the highest reach-to-effort ratio and can be shipped without changing core underwriting economics.

Recommended Solution

Ideas are split by execution ambition first. The final prioritization is applied only to Moonshot ideas because those are the strategic bets that need a clear PM decision framework.

OK Ideas

Best Ideas

Moonshot Ideas

Solution Prioritization

Solution Discussion

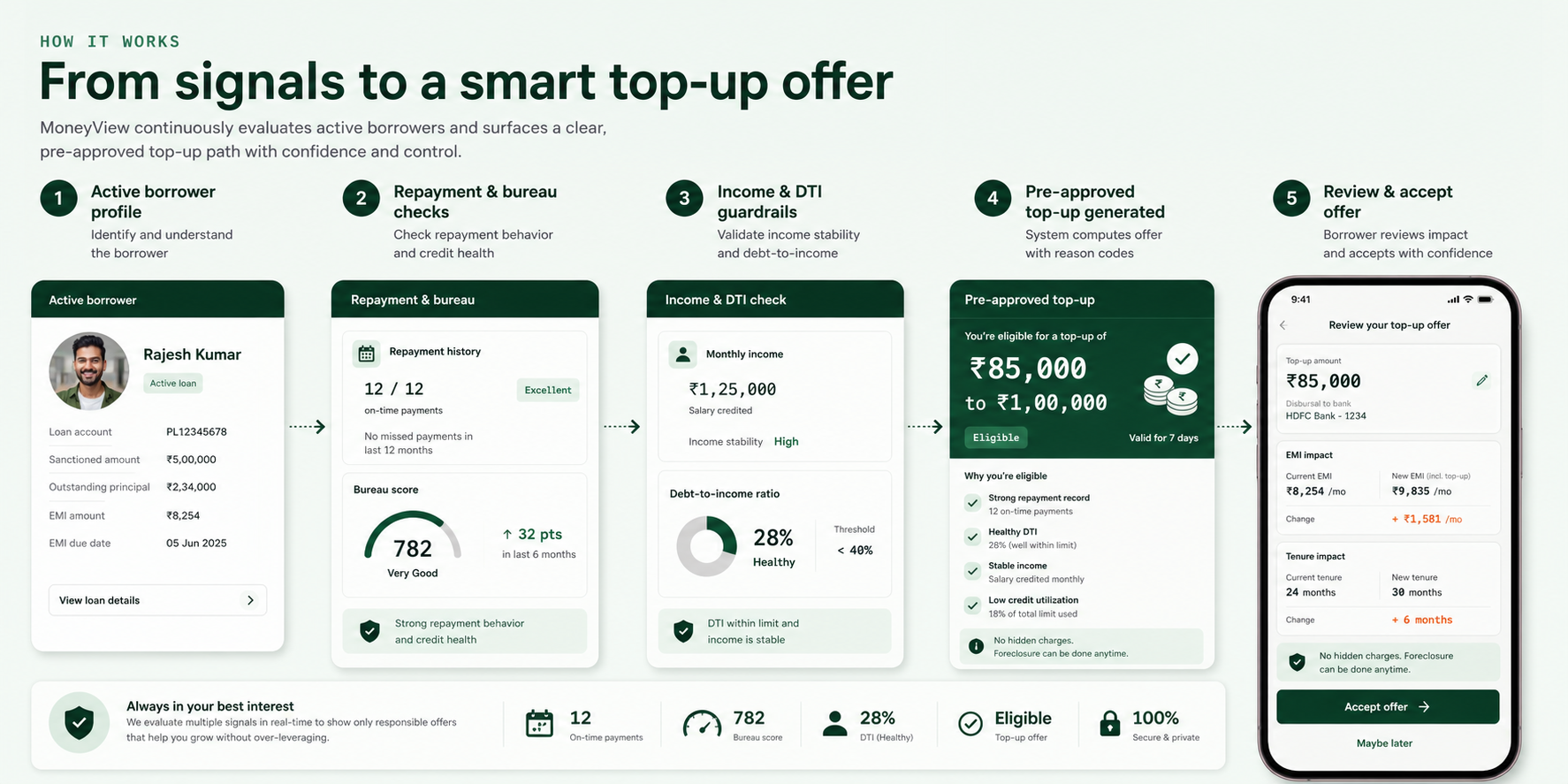

Selected solution: Autonomous credit path advisor. The product should continuously explain whether an active borrower is ready for a top-up, what is blocking them, and what action improves eligibility.

A decision layer that turns repayment behavior, bureau quality, income signals, and lender policy into a clear next-credit path.

- Ingest

Read repayment history, outstanding principal, bureau score, income proof, DTI, and lender-policy constraints.

Data contract: borrower_id, active_loan_id, policy_version. - Decide

Run policy rules plus advisor logic to classify eligibility state, blockers, amount range, and next eligible date.

Decision contract: eligible, reason_code, confidence, max_offer. - Surface

Show amount range, reason codes, EMI delta, offer expiry, support-safe explanation, and responsible top-up CTA.

UI contract: status card, detail drawer, calculator, CTA. - Learn

Track acceptance, rejection reasons, support calls, default, repeat retention, and reason-code accuracy.

Feedback loop: weekly cohort review and rule tuning.

Dashboard card, eligibility badge, explainable blockers, EMI impact view, and one-tap top-up CTA.

- Status badge

- Reason drawer

- EMI simulator

Eligibility API, policy engine, feature store, reason-code mapper, offer generator, and audit log.

- Policy engine

- Offer generator

- Audit trail

DTI ceiling, bureau threshold, lender policy checks, consented data use, and adverse-action explanation.

- DTI limit

- Bureau threshold

- Consent logs

Lower failed applications, lower support dependency, healthy default rate, and higher repeat retention.

- 10% pilot

- Default guardrail

- Retention lift

Implementation Plan

Launch the advisor as a controlled risk pilot: build explainable eligibility decisions first, then expose them through borrower, support, and risk-review surfaces.

Filter borrowers with running loans, EMI history, income proof, and bureau refresh.

Policy rules, DTI guardrails, reason-code mapper, and next-eligible-date logic.

Converts decisions into borrower-safe guidance, top-up range, and next best action.

Top-up CTA, support console, audit log, disbursement, and repayment restructure.

Eligibility API, feature store, policy versioning, reason-code taxonomy, and offer generation.

Owner: Risk + BackendDashboard card, top-up calculator, reason drawer, EMI delta, and responsible CTA states.

Owner: Product + AppAgent console, shared reason codes, escalation paths, pilot queue, and borrower education scripts.

Owner: Ops + CXFinalize policy inputs, data contract, and top-up states.

Decision API, advisor copy, app card, and support console.

Backtest eligibility, QA reason codes, and review compliance copy.

Launch to 10% eligible cohort with default and support guardrails.

Expand after approval quality, DTI, default, and retention checks.

Risk: default rate below threshold and DTI impact controlled.

Product: fewer failed applications and lower support dependency.

Business: repeat-borrower retention lift and healthy top-up conversion.

Success Metrics

Metrics must prove that the advisor improves repeat-borrower clarity without creating risky credit growth. The North Star combines usage, successful top-up completion, and portfolio safety.

Percentage of eligible active borrowers who view the advisor, understand their next credit path, complete a responsible top-up, and remain within portfolio risk guardrails.

Advisor viewed → reason understood → calculator opened

>30%Shows borrowers are seeing and understanding the next-credit path.

Explanation trust and low drop-off before CTA.

Eligible borrower accepts advisor-recommended top-up path

15-25%Measures whether guidance turns into responsible repeat credit.

Completion rate stays at 85-90% after acceptance.

Default, DTI movement, delinquency, and early repayment stress

<5%Prevents growth from becoming risky credit expansion.

DTI increase stays below +10% and no policy breach.

Repeat retention, incremental revenue, reduced lender switching

>70%Confirms MoneyView keeps good borrowers instead of losing them.

Revenue target ₹5-10 Cr without default deterioration.

GTM

Launch should start inside the active borrower base, not through broad acquisition. The motion is in-app, eligibility-triggered, support-aware, and guarded by portfolio health checks.

Users with clean EMI behavior, verified income, and a clear repeat-credit need.

Notify when repayment behavior unlocks a top-up path or a next eligible date.

Dashboard card, push notification, WhatsApp reminder, and support-agent script.

Limit launch by DTI, default early-warning signals, lender policy, and cohort health.

Budget Allocation

Run advisor daily for active borrowers.

Show eligibility card to 10% controlled cohort.

Trigger top-up offer only when risk gates pass.

Expand by default, support, retention, and revenue checks.

Summary

The teardown identifies a product clarity gap in MoneyView's repeat borrowing journey and turns it into a prioritized solution, rollout plan, metrics system, and GTM motion.

Good borrowers do not know if, when, or why they can access another responsible credit path.

A strong-credit active borrower proves the issue is clarity, not simply borrower risk.

Explain eligibility state, blockers, amount range, EMI impact, and next best action.

Build decision service, borrower UI, support console, launch gates, and cohort monitoring.

MoneyView should proactively show responsible active borrowers a transparent next-credit path before they leave for another lender or take a higher-risk borrowing option.